Most money advice fits people who already have extra money. You may not have that space. You deal with tight monthly income. Money planning feels like pulling water from a dry sponge. Zero-based budgeting changes that. Not because it's magic but because it forces every dollar to work instead of disappearing.

That's why here's what it actually looks like when your income is low, your expenses are real, and you can't afford to guess.

Let's go through it in detail.

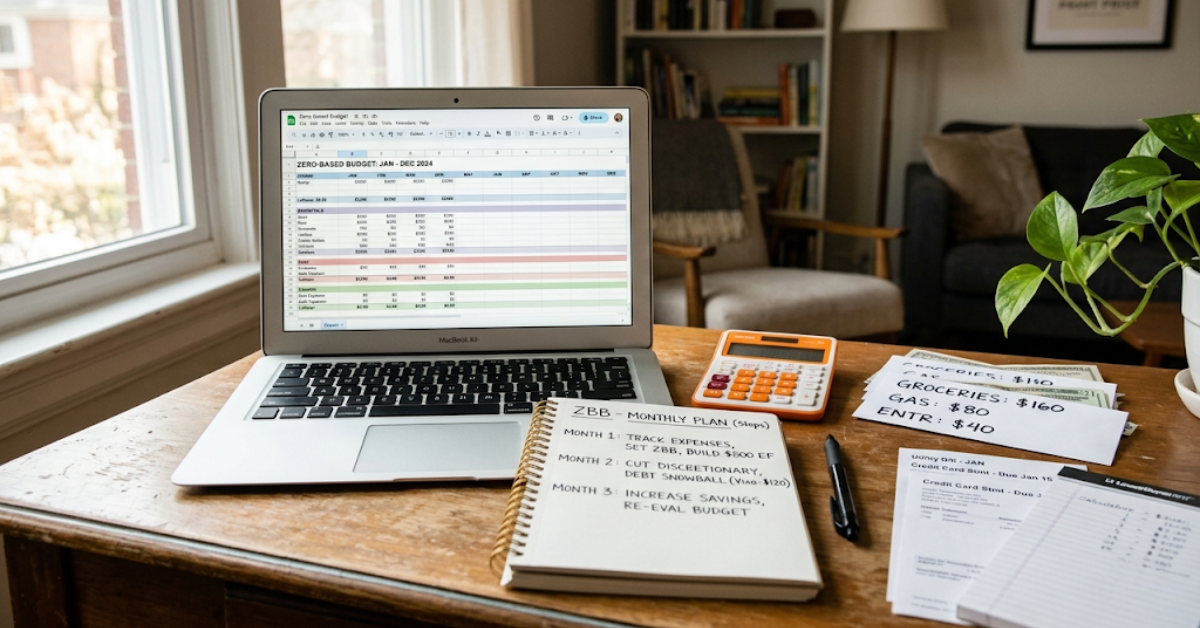

1 What Zero-Based Budgeting Actually Means?

Zero-based budgeting means you allocate every dollar of your monthly take-home pay toward expenses, savings, and debt payments. Your income minus your expenses should equal zero.

That does not mean you spend everything, savings count as an expense. Debt payments count. Your emergency fund contribution gets a line. So, the idea is simple: every paycheck dollar is first assigned to a category: bills, sinking funds, extra debt, groceries, fun. Leftover money is not allowed. So, you must give it a job. Right?

Why does this matter when you're on a low income? Because vague money disappears. If $200 has no name, it evaporates in two weeks and you have no idea where it went. If it's labeled groceries, you protect it.

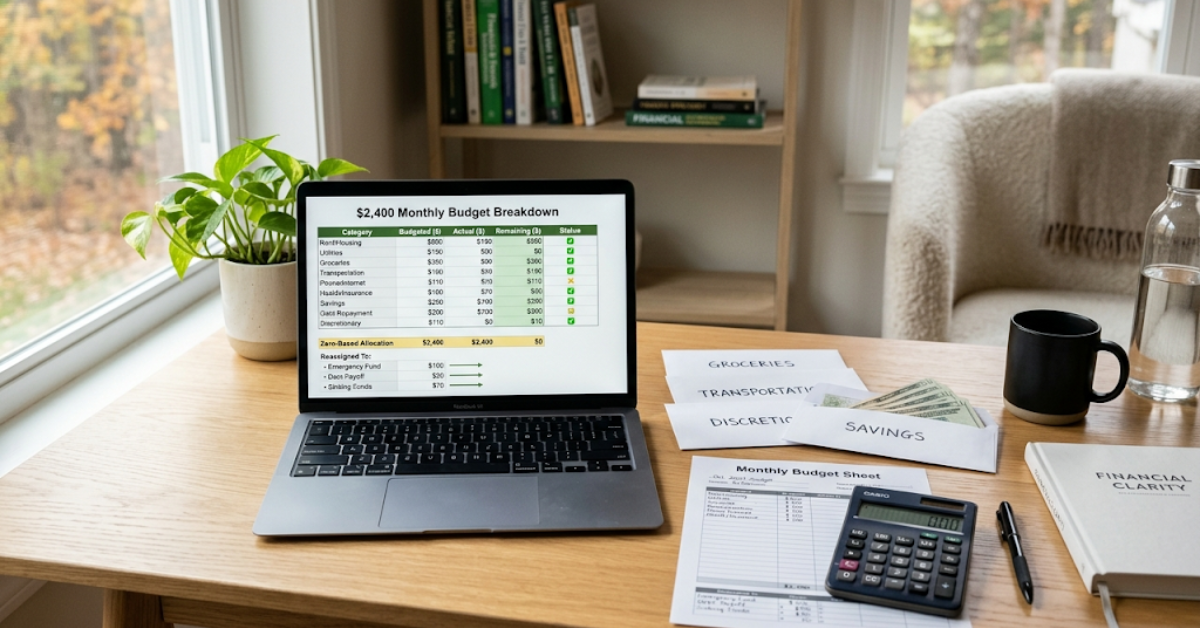

2 Now The Real Numbers: A $2,400/Month Budget

Okay let's use a real scenario. You take home $2,400 a month that's roughly $29,000/year after taxes. Single adult, one city, renting. Only 32% of people earning under $25,000 spend less than what they earn. That number jumps to 66% for people earning $100,000 or more. That gap is not about discipline. It's about margin.

So Zero-based budgeting is how you manufacture margin even when it doesn't feel like it exists. Well here's how the $2,400 breaks down:

Month 1 Budget Zero-Based

Now wait that leaves $600 unassigned. That's the point. Now you assign it. You put $200 toward the emergency fund. Put $200 toward extra debt payoff. And put $100 toward a sinking fund (car repair, medical, whatever irregular expense hits you hardest). Put the last $100 toward next month's rent buffer so a tight week doesn't destroy you.

Now you're at zero. So every dollar has a name.

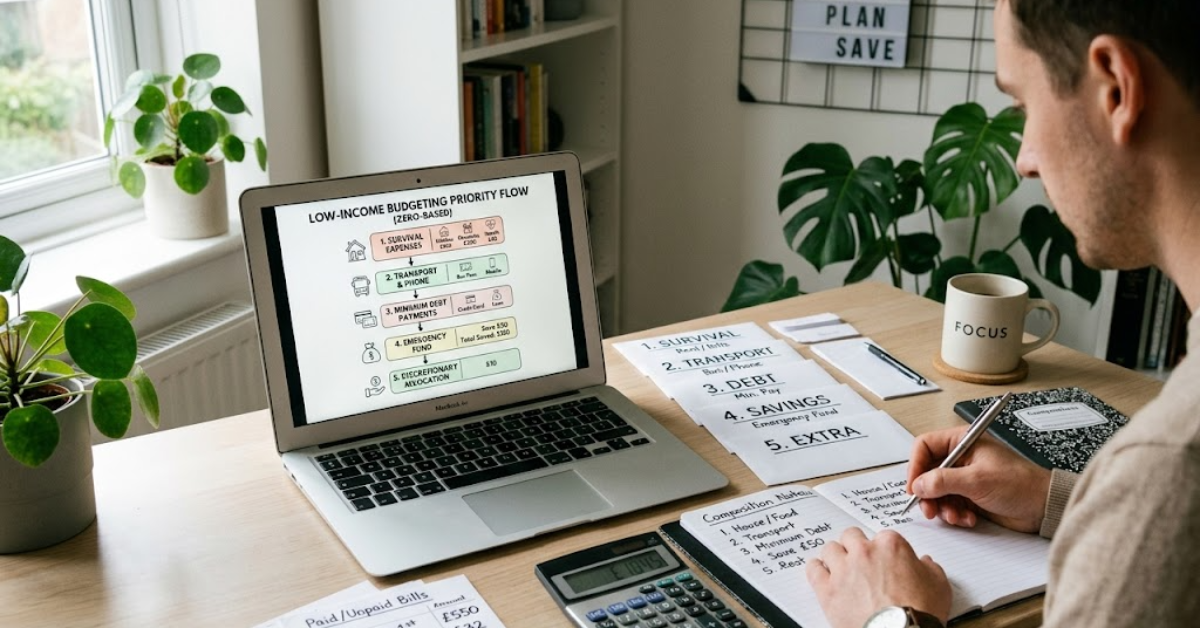

3 How to Actually Allocate: The Priority Order?

If income is low, you cannot treat all expenses equally. That's why I use this order every single month.

Cover your survival line first. Rent, utilities, and groceries stay must-pay expenses. Cover these first before anything else. For the $2,400 example, the total comes to $1,310. It goes first. Always.

Transportation and phone. You need to get to work. You need your phone to apply for jobs, call your employer, and manage your accounts. So these go second. Another $165.

Minimum debt payments. Okay missing minimums destroys your credit and triggers fees. Pay them. Don't skip. In this budget, $80.

So a tiny emergency fund contribution. Even $25 counts. And a starter emergency fund of $500 to $1,000 is the realistic first milestone. Reaching $500 first creates momentum and removes the psychological barrier of the larger number. Start with what you have.

Assign what's left. Debt payoff, sinking funds, fun money in that order.

At $4,000/month, there's not a lot of margin for error. The key is honesty about what you actually spend. Most people underestimate groceries and dining out by 20–40%. At $2,400, that honesty is even more critical. Round up your estimates, not down.

4 Month 1: Set the Foundation

Your first month is about accuracy, not perfection. Track every purchase. You use a notes app, a notebook, or Google Sheets to track your money. Whatever you'll actually open. Many budgeting platforms now include AI-powered projections which helps you see how reallocating $50 today could affect your savings six months from now. But you don't need an app. Paper works.

At month end, compare what you planned vs. what happened. You'll probably overspend in one category and underspend in another. That’s normal that you spent $50 extra on groceries? No stress. Move $50 from clothes or fun money instead. So, the total still stays zero.

Do not restart from scratch. Adjust and keep going.

5 Month 2: Build the Emergency Fund Habit

Now a 2025 Federal Reserve report found that 63% of adults would have difficulty covering an unexpected $400 expense. You don't want to be in that group. Month 2 goal: get your emergency fund to $100. That sounds small. It is. But it's real. Here's how you do it without feeling it:

Automatic transfer. Set a $25 automatic transfer on payday. You won't miss it if it moves before you see it. Small, consistent contributions add up to $260 a year on a $5/week plan, more than half the starter fund goal.

Cash-back apps help you earn money back on things you already buy. Apps like Ibotta and Fetch Rewards give you cash or points when you shop for groceries.. Redirect every payout to savings.

Sell one thing. A clear-out of unused clothes or electronics on Facebook Marketplace can generate a one-time $100–$500 boost toward the starter fund goal.

You should keep the emergency fund in a separate account. Not your checking. Not your debit card. Somewhere you have to consciously move money from. You want access within 1–2 business days not instantly, but not locked away either. You see now by Month 2, target: $100 in emergency savings.

6 Month 3: Tackle the Irregular Income Problem

Maybe you have a side hustle. Maybe your hours vary. One paycheck gives $1,900. Next paycheck gives $2,700. Low-income budgets break here. You plan for the $2,700 month. Then the $1,900 month hits hard. Zero-based budgeting actually handles this well. Now here's the rule:

Always budget from your lowest expected month.

Okay for variable income: use your lowest expected monthly income as the baseline. If you made $1,900 last month and $2,700 the month before, budget on $1,900. If extra comes in, give it a job immediately. So here's a real split for a $500 windfall month:

Extra Income Usage

None of it floats. None of it becomes "spending money." Every dollar gets assigned the day it arrives. Last month they brought in $8,200 after covering the base, the extra $2,700 was assigned exactly according to the rules. Zero left over, zero guesswork.

7 Month 4: Add a Sinking Fund

See here's what wrecks low-income budgets more than anything: irregular expenses. Your car needs a tire. Your phone screen cracks. A medical bill shows up. So these aren't emergencies, they are predictable surprises. And they shouldn't drain your emergency fund.

A sinking fund is just a savings bucket for a specific future expense. You add $20–$40 a month. If the expense hits, the money is already there. Start with one.

Car repairs: save $30/month → $360/year ready

Medical copays: save $20/month → $240/year ready

Annual subscriptions or fees: save $15/month → $180/year ready

Add it to your budget as a line item. Sinking fund categories prevent the irregular expenses that derail most budgets. Treat it like rent non-negotiable. Month 4 target: one sinking fund running, emergency fund at $200+.

8 Month 5–6: Start Seeing the Shift

By Month 5, something changes. You stop reacting to your money and start directing it. 67% of Americans were living paycheck to paycheck in 2025. Zero-based budgeting is specifically designed to break that cycle not by earning more, but by closing the gap between money in and money accidentally spent.

Here's what Month 5–6 looks like with the same $2,400 income if you've stayed consistent:

Month 6 Snapshot

Still $400 short of zero? Assign it. Split it between emergency fund and extra debt. Or bulk up the sinking funds. Hit zero. Notice the emergency fund is now at $100/month instead of $50. The debt extra payment doubled. That happens naturally when you stay consistent and tighten variable spending.

9 The Real Rules for Budgeting on Low Income

People have already used these habits and seen them work in real life. Check your budget every week, not just once a month. Monthly reviews often come too late to fix mistakes. Spend 10 minutes every Sunday on your spending. You spot problems early. You fix small issues before they grow. You stay on track with your money. Now use simple rounding. Also keep it practical.

Round expenses up. Round income down.

Groceries cost $265? Set $285. Paycheck comes $2,400? Plan $2,300. The buffer protects you. Name every dollar the day money arrives. Once the plan is set, you track spending against those category limits, adjusting only when new income arrives or priorities change. Don't let extra income sit unnamed for even 24 hours.

Keep some fun money, even on $2,400 a month. Even $40 a month helps you stay balanced. It stops that all-or-nothing mindset that ruins budgets. No breathing room in budget makes you quit it fast. Keep the emergency fund separate. Don’t touch it for wants.

10 What to Do When the Budget Breaks?

It will break. That's not failure — that's life. Your car breaks down. Your hours get cut. An unexpected bill shows up. Here's the response protocol:

Pause all sinking fund contributions for that month

Redirect fun money and miscellaneous to the problem

Use your emergency fund if the expense qualifies

Rebuild the emergency fund starting next month, even if it's just $25

Make a plan for times when variable monthly bills such as electricity might run higher than normal. In these cases, you may need to take funds from one area, such as entertainment, to maintain the zero balance. The budget doesn't restart from scratch. It absorbs the hit and adjusts. That's the entire advantage over not having a budget at all.

11 Well, The Honest Part Nobody Tells You

Zero-based budgeting can help you stay in control of your money. Still, it takes effort when your income barely covers your monthly expenses. So the math is tighter and the margin for error is thinner. But here's the thing: a tight income with a plan beats a tight income without one every single time. You don't need to earn more to start.

You need to know where the money goes. Once you know that, you can make decisions instead of discovering consequences. Month 1, you get organized. Month 3, you stop dreading payday. Month 6, you have a real emergency fund for the first time. That's not nothing. That's the whole point.

Start with next month's income number. List your expenses. Assign every dollar. Hit zero.

Snober Kanwal

Tech Reviewer, Content SpecialistI specialize in tech journalism and product reviews at CouponsBeast. By breaking down digital trends, gadgets, and software into easy-to-digest guides, I create SEO-optimized content that ranks on search engines, builds consumer trust, and drives high-intent affiliate traffic for global audiences.

Comments 0

No comments yet. Be the first to share your thoughts!